This article is the original work of EMO Capital and requires permission for reprinting and citation.

Key Takeaways:

- Integration of RWA and DeFi: The tokenization of Real-World Assets (RWAs) brings the assets of the physical world into decentralized systems, enhancing their accessibility, liquidity, and transparency, thus building a bridge between traditional finance and decentralized finance.

- Current State of the RWA Market: Although the RWA market is growing quickly, its penetration rate is still low compared to traditional assets, meaning that even a slight increase in penetration could lead to rapid market expansion.

- Growth Drivers of RWA: The rapid growth of RWAs is propelled by several factors, including bringing stability to the DeFi ecosystem, improving the liquidity and transparency of non-standardized assets, and reducing transaction costs.

- Future Trends and Investment Opportunities: The RWA market is expected to reach a size of $1.8 trillion by 2030, indicating substantial growth potential. Attracting more traditional investors will be key, while also establishing a regulated and traditional finance-friendly framework is necessary.

- Technical and Regulatory Challenges: Current on-chain data still cannot fully mitigate counterparty risks in the transaction process, and there is regulatory uncertainty. Further technological innovation and legislative improvements are needed to address these issues.

1. What is RWA:Link between real world and crypto

RWA “DeFi-ing” real world into decentralized system. Real-world assets (RWAs) are tangible or intangible assets that exist in the physical world, such as financial assets, real estate. They can be tokenized and brought onto the blockchain, which means that their ownership rights are mapped to tokens in the DeFi ecosystem. This process is called RWA tokenization.

Tokenized RWAs can be used in conjunction with DeFi protocols to connect centralized and decentralized systems, effectively “DeFi-ing” real-world assets. This means that RWAs can be fractionalized, traded, and lent on DeFi platforms, which can make them more accessible and liquid.

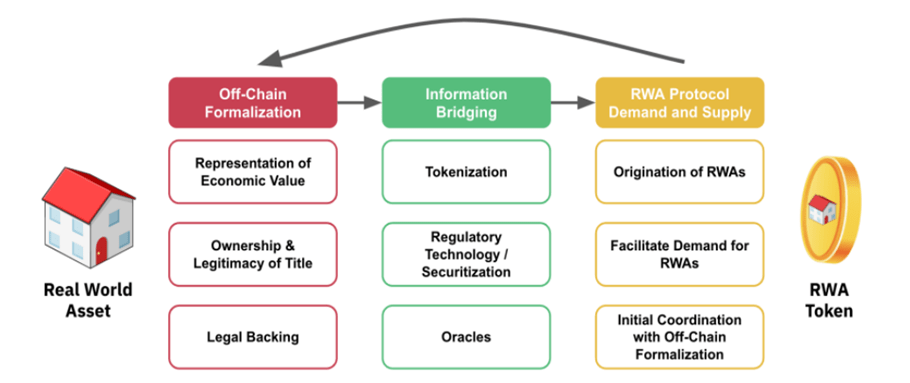

Figure: Tokenization of Real-World Asset

Source: Binance Research,, EMO Capital

RWA tokenization process: integrate real-world agreements with smart contract protocol and on-chain data. Integrating RWA into the DeFi ecosystem generally involves standardizing and clarifying external information from off-chain sources, including the economic value, ownership, and legal protection of asset rights associated with the RWA, as shown in following steps:

- Standardizing and Clarifying External Information: which include economic value assessment, ownership verification and define legal rights for underlaying asset and involving parties.

- Data Onboarding and Integration: which include digitization of real data and store data in to on-chain blocks.

- DeFi Protocol Integration: which include integration of RWA data with DeFi protocol and smart contract functions, to ensure the process of trade and ownership transfer align with legal agreements set up before.

Integrating RWAs into DeFi opens up a world of possibilities, enhancing asset accessibility, liquidity, and transparency. By bridging the gap between traditional and decentralized finance, this innovative approach can revolutionize the way real-world assets are managed and utilized.

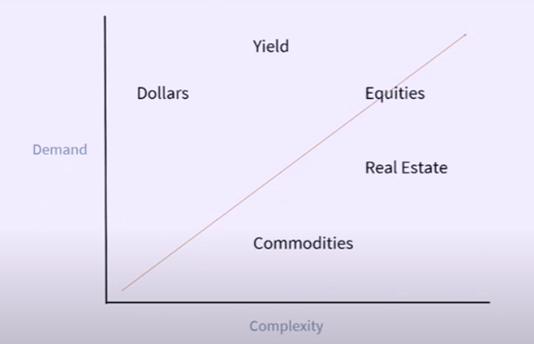

Asset type of RWA including major financial assets and non-standardized assets. In theory, as long as tokenization can be achieved through compliance means, any asset in the real world can become a potential target for the development of RWA. At the current stage, the main asset categories for RWA can be roughly divided into two types: 1) Financial assets that are subject to strong regulation (such as currency, stocks, bonds, etc.); 2) Non-standardized assets that are subject to less regulation (such as real estate, private credit, art collections, etc.).

For financial assets such as currency, stocks, and bonds that are subject to strong regulatory oversight, the main drivers of tokenization are service providers with strong regulatory endorsement and traditional financial institutions exploring the crypto field. The emergence of related products provides DeFi traders with better trading and collateral assets besides native crypto assets, which will contribute to the continuous growth of the DeFi scale and the innovation of trading forms.

For non-standardized assets with less regulatory oversight, such as real estate, private credit, and art collections, their tokenization is mainly driven by innovative service providers. On-chain can bring sufficient liquidity to these assets, while the security of on-chain transactions also greatly reduces the transaction costs of these assets, improving transaction efficiency.

Figure: Tokenization Framework by Asset Type(Sort by Demand and Complexity)

Source: Messari, EMO Capital

2. Current State of RWA:At the early stage of fast growing

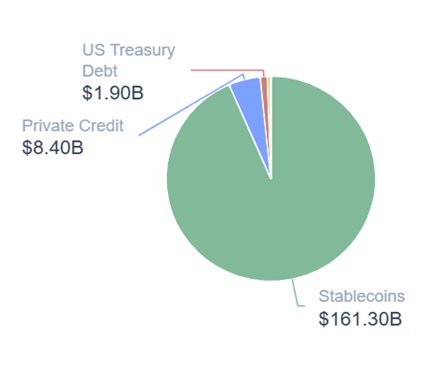

RWA sector experiencing radical growth on both on-chain value and active user basis, counting for $11 B in total value and 60m users. According to data from RWA.xyz, the aggregate on-chain value of Real-World Assets has reached a substantial $173 billion. Notably, stablecoins dominate this figure, constituting over 90% of the total, amounting to approximately $161 billion. When factoring out the contribution of stablecoins, the remaining on-chain value attributed to RWA is $11 billion, which has experienced a month-over-month increase of 6.83%.

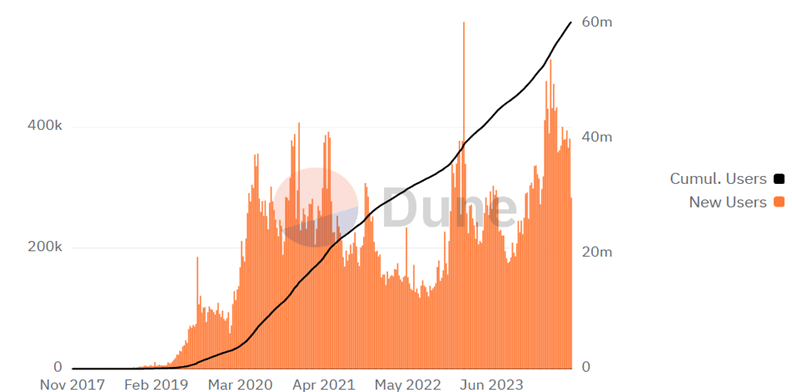

In terms of user engagement, the RWA sector has demonstrated a sustained growth trajectory in recent years. Data from Dune Analysis indicates that the cumulative user base within the RWA sector has expanded to an impressive 60 million. The trend of new user acquisitions has been consistently upward, reflecting a robust interest and participation in the RWA space.

Figure: Total RWA On-chain value by Type (Include Stablecoin)

Source: RWA.xyz, EMO Capital

Figure: Number of Users that are Currently Holding or Previously Held a Tokenized Asset

Source: Dune Analysis, EMO Capital

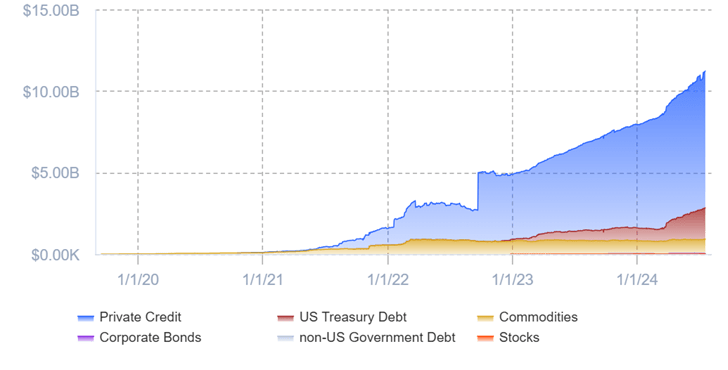

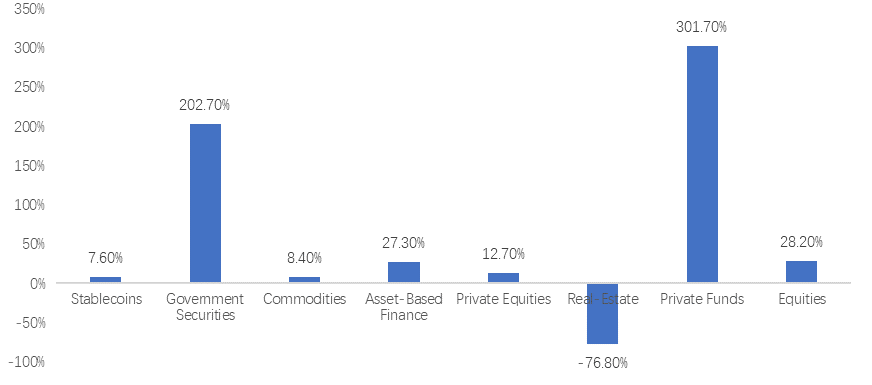

Asset Segments: Private Credit and Government Bond contribute the main driven force of growth. According to data from RWA.xyz, excluding stablecoins, the tokenization scale of RWAs in the Private Credit and US Treasury Debt categories has shown a rapid upward trend in recent years. The current overall scale of these assets is $8.4 billion and $1.9 billion, respectively. Additionally, the Commodity category has maintained a stable scale, currently at $0.9 billion. Based on data from Dune Analysis, the annual growth rates of market value for Fiat-Collateralized Stablecoins, Government Securities, Commodities, Asset-Based Finance, and Equities are 7.6%, 202.7%, 8.4%, 27.3%, and -28.2%, respectively.

Overall, excluding stablecoins, the application of RWA tokenization is most extensive in the private credit sector. The tokenization processes in areas such as government bonds, stocks, and commodities are still in the early stages of rapid development. The potential for further growth in these areas is significant, as the benefits of tokenization, such as improved market access, enhanced liquidity, and reduced transaction costs, become more widely recognized.

Figure: Total RWA On-chain Value Growth (Exclude Stablecoin)

Source: RWA.xyz, EMO Capital

Figure: YoY Growth by Segments in RWA

Source: Dune Analysis, EMO Capital

Protocol Segments: While major players exhibit some differences in business models, the competitive landscape remains undefined due to the rapid development stage of the market.

Currently in RWA sector exists two categories of major players, one is the service providers on different asset class (e.g. Centrifuge, Maple), the other is institution who integrate RWA into their protocol (e.g. Maker DAO, Aave). They perform the role of sell side and buy side in the existing RWA ecosystem.

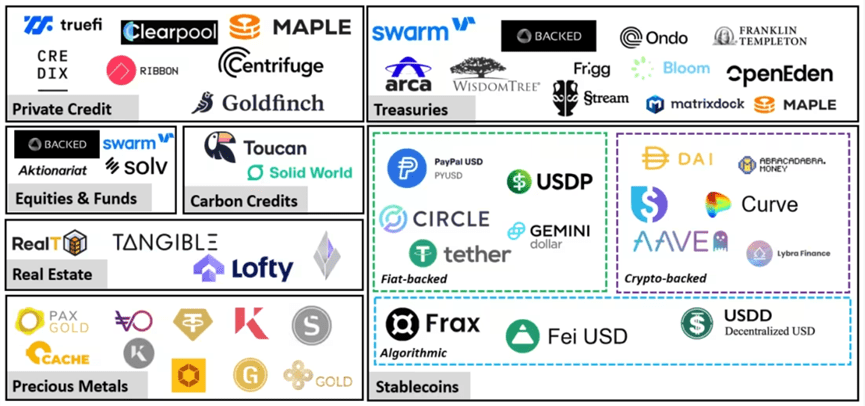

Figure: RWA ecosystem map

Source: Galaxy Research, EMO Capital

The main RWA service providers can be categories by asset classes:

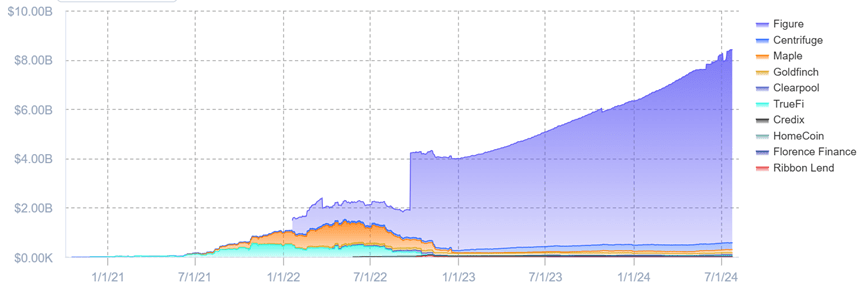

1) Private Credit: As the most developed sector in RWA, major players each has some unique feature. Centrifuge (largest issuer in this sector, one of the first protocols s to integrate trenching natively into its contracts), Goldfinch (focus on emerging market, use a unique community -determined underwriting mechanism), Maple.

Figure: Competitive landscape for private credit products (including Figure)

Source: RWA.xyz, EMO Capital

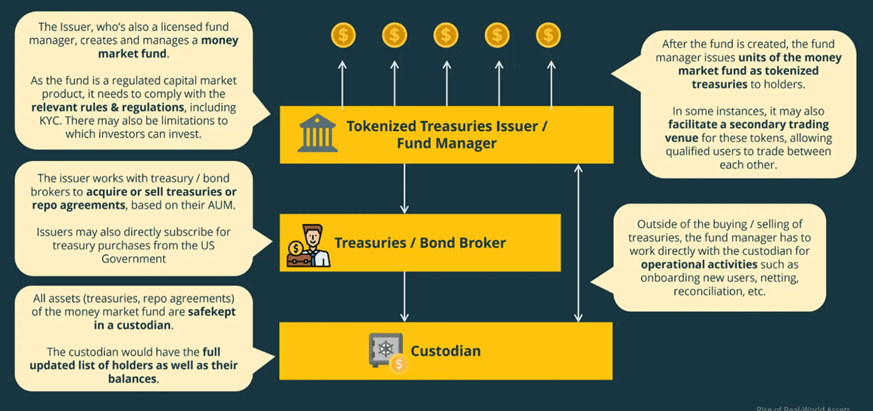

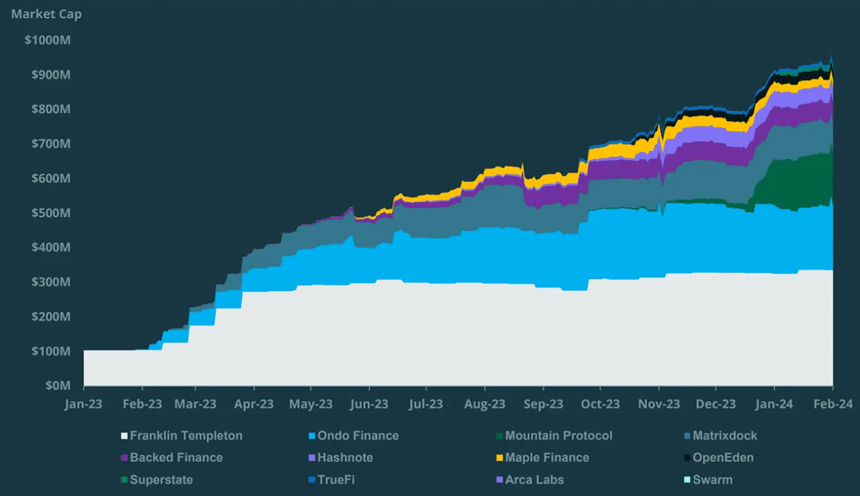

2) Government Bond: Typical tokenized Treasuries product involve Issuer/Broker/Custodian, where Broker and Custodian are ran by traditional financial institution, while major Issuers include TradFi giants like Franklin Templeton and Wisdom Tree, crypto native players like Ondo Finance, Matrix Dock,

Figure: Typical structure for tokenized treasuries product

Source: CoinGecko, EMO Capital

Figure: Competitive landscape for tokenized treasury products

Source: CoinGecko, EMO Capital

3) Real Estate: RealT Tokens is the biggest issuer of tokenized real estate with a 49% market share. Tangible, another real estate focused RWA issuer, has seen the strongest growth in recent years.

And for institution who integrate RWA, we take Maker DAO as example:

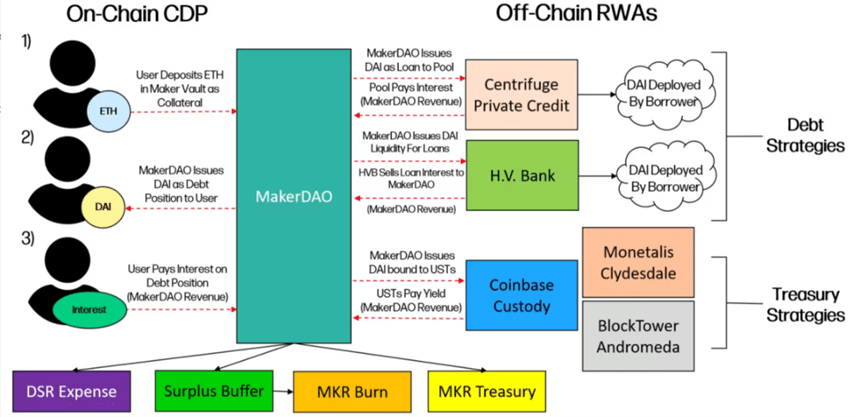

RWA become a desirable asset as collateral to back its stablecoin DAI. Maker DAO’s RWA strategy is part of a larger initiative to build a resilient, decentralized, and revenue-generating stablecoin. To achieve this, the protocol has on-boarded multiple types of RWAs and RWA strategies according to different terms, sources, and processes. This was done intentionally in accordance with the DAO’s goal of diversifying the backing of DAI to the greatest extent possible. The RWAs captured by Maker DAO all generate yield that accrues to the DAO as revenue. In fact, nowadays Maker Dao’s revenue from RWA asset even larger than its revenue from minting DAI (which called stability fee).

Figure: Maker DAO implementation of RWA

Source: Galaxy Research, EMO Capital

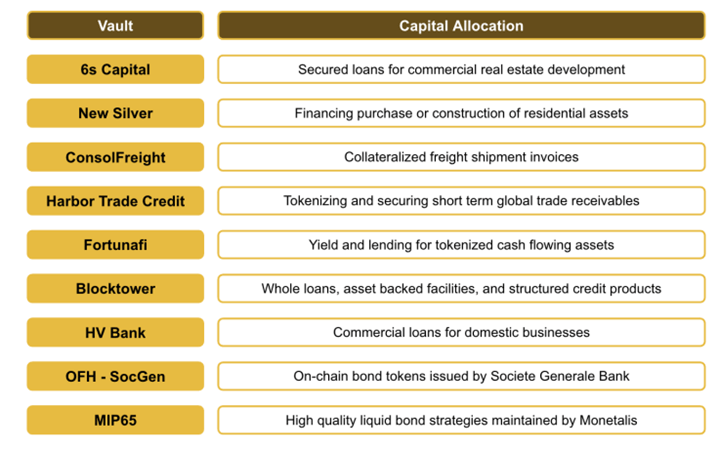

The Collateral Vaults of Maker DAO comes from different TradFi institutions. The majority of Maker DAO’s RWA collateral comes in the form of US treasury bonds managed by Monetalis (MIP65). Maker DAO also launched a vault backed by US$100M worth of loans originating from a community bank in Philadelphia called Huntingdon Valley Bank (“HV Bank”). HV Bank used Maker DAO to support the growth of its existing businesses and investments around real estate and other related verticals, and served as the first commercial loan participation between a US-regulated financial institution and a decentralized digital currency protocol. In a separate vault, French multinational banking giant, Société Générale borrowed US$7M from Maker DAO in a position backed by €40M worth of AAA-rated tokenized bonds.

Figure: Different borrowers from Maker DAO’s RWA collateralized vaults

Source: Binance Research, EMO Capital

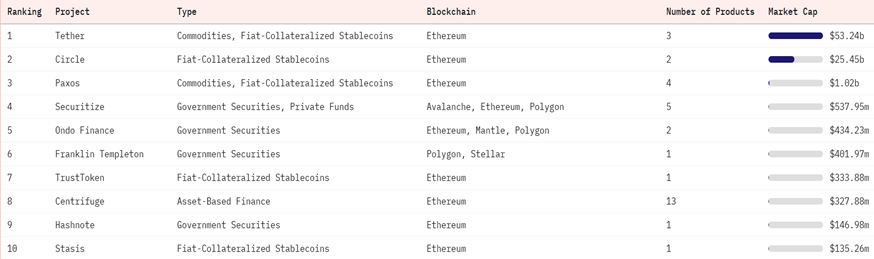

Chain Segments: Ethereum still prevail, while other chains also show growth potential. The current mainstream RWA projects predominantly opt for deployment within the Ethereum ecosystem, leveraging its extensive infrastructure and robust community support. However, other blockchain platforms such as Polygon, Mantle, Avalanche, and Stellar have been garnering attention for their distinct advantages, leading to a multi-chain strategy adoption among some projects.

For instance, Ondo Finance has chosen a multi-chain approach, utilizing Ethereum, Mantle, and Polygon to enhance accessibility and scalability. This strategy allows Ondo Finance to benefit from the security and decentralization of Ethereum while also leveraging the high throughput and lower costs associated with Polygon and the innovative features of Mantle. In another noteworthy move, the traditional finance giant Franklin Templeton has shown preference for Polygon and Stellar. Polygon’s Layer 2 solution offers a scalable and cost-effective alternative to Ethereum, making it an attractive choice for projects seeking to reduce gas fees and improve transaction speeds. Stellar, on the other hand, is known for its focus on cross-border payments and remittances, featuring a stable and energy-efficient network that is well-suited for certain types of RWA applications.

Table: Summary of the Tokenized Assets by Project

Source: Dune Analysis, EMO Capital

3. RWA Growth Driven Force: Liquidity, transparency and stability

The rapid growth of RWA is driven by multiple factors form different stakeholder within this industry, all of these will jointly drive RWA sector’s future growth:

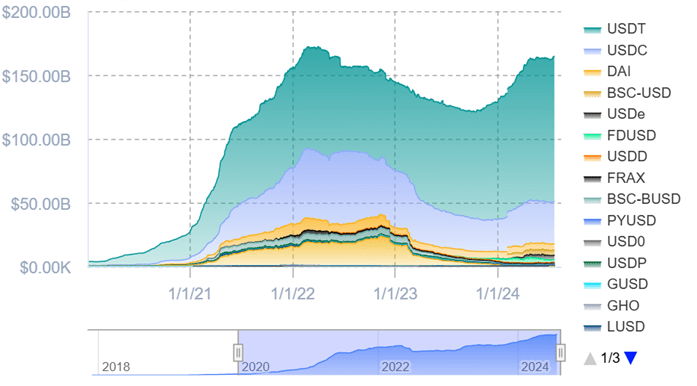

From Crypto Side: Introducing real world asset into DeFi can help stabilizing DeFi ecosystem. As the transmission mechanism in the DeFi ecosystem is more complex, widely connected, and faster than in traditional finance, the price performance of major collateral assets, LP trading pair assets, and project tokens is crucial for the health of the DeFi ecosystem.

When major cryptocurrency (BTC, ETH, etc.) prices fall rapidly, it exacerbates the liquidation of collateral in lending contracts. This liquidation can further lead to market sell-offs, potentially pushing prices down further. Meanwhile, rapid declines in major coin prices can also lead to price declines in DeFi project tokens. This can, on the one hand, lead to a decrease in the project’s TVL and thus lower project yields, causing user asset outflow. On the other hand, the outflow of user assets can lead to leveraged borrowing funds entering a concentrated liquidation phase, which puts further downward pressure on prices. To avoid such systematic risk existed within DeFi, new asset (to crypto) which nature is uncorrelated with major coins is necessary. Example as the rapid volume growth of stablecoin in recent year, provide crypto investor a good tool to mitigate such volatility.

In conclusion, introducing real-world assets as collateral in DeFi can reduce the overall volatility of the DeFi ecosystem and enhance its stability.

Figure: Total market cap of stablecoins, more RWAs on the way

Source: RWA.xyz, EMO Capital

From Asset Provider Side: RWA Tokenization provide liquidity and transparency while reduce trading cost. Tokenization offers a promising solution to enhance the liquidity of non-standardized assets, particularly in the realms of private credit, real estate, and art collections. 1)Tokenization streamlines the trading process by eliminating intermediaries and automating transactions, significantly lowering costs and time spent on traditional market transactions. 2)By leveraging blockchain technology, tokenized assets can benefit from enhanced transparency and accessibility of information, fostering trust and reducing counterparty risk. 3)Tokenization opens up global markets for non-standardized assets, attracting a broader pool of potential investors and enhancing liquidity. Overall, tokenization presents a transformative approach to unlocking the liquidity potential of non-standardized assets, facilitating efficient and inclusive access to these investment opportunities.

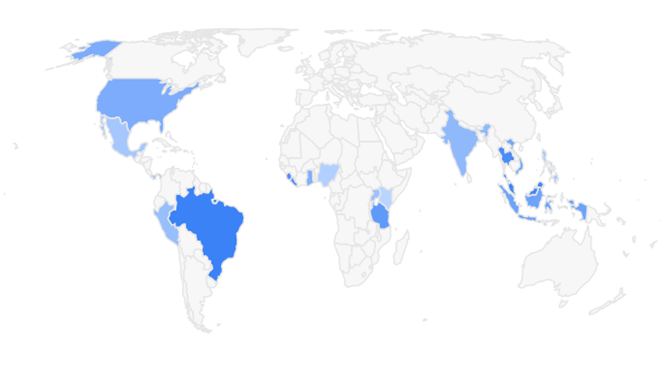

Take Private Credit RWA as example, the end borrowers are mainly come from under-developing area and emerging market like SEA, Africa or India, which are mainly caused by the financial market in these regions are less developed, leaving many small-to-medium sized businesses without access to traditional banking or capital markets. Besides accessibility, on-chain also reform collateral management process, the collateral is not held by a custodian, but instead, is controlled and managed by the smart contract. Unlike traditional collateral management, which requires time-consuming processes and manual intervention (for example, T+2 cash settlement), the management of collateral through smart contracts can occur near-instantaneously through preset conditions. Incorporating smart contracts in finance could shorten margin cycles, reduce collateral requirements, lower credit line utilization and therefore lower capital costs.

(Should be notice that this feature only for assets with less liquidity and disclosure, liquidity improvement show less effect on standardized asset class like bond or equity.)

Figure: Location of end borrowers of private credit RWA

Source: RWA.xyz, EMO Capital

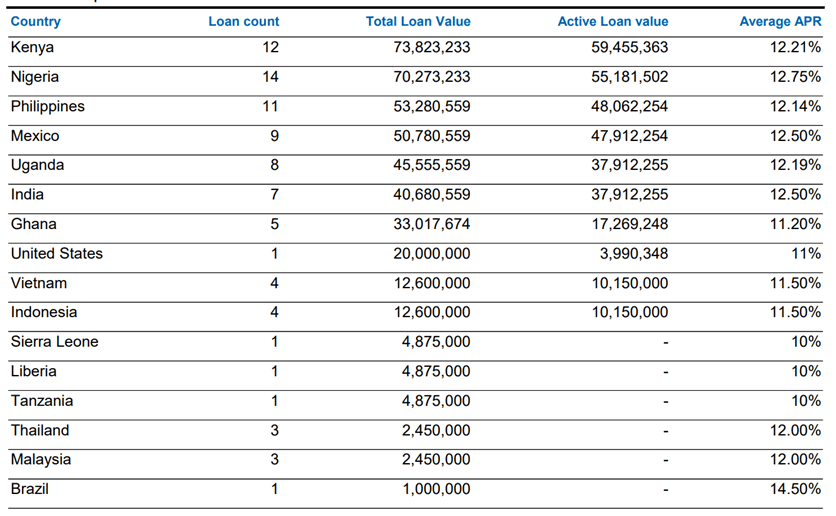

Table: Distribution of private credit loans across countries

Source: RWA.xyz, EMO Capital

From Service Provider Side: RWA provide TradFi giants a chance to leverage their influence in crypto world. RWA offer a strategic opportunity for TradFi giants to leverage their existing strengths and establish a foothold in the crypto world, whereas they may less competitive with crypto-native players in other fields. By embracing this new technology and asset class, they can potentially expand their reach, enhance their offerings, and contribute to the overall growth and maturity of the crypto ecosystem.

But one thing should be noticed that TradFi giants are not the only players in the field of RWA, many tech companies (e.g. Oracle) and crypto-native institution (e.g. MakerDAO) also contribute to the building of infrastructure and model innovation within this sector.

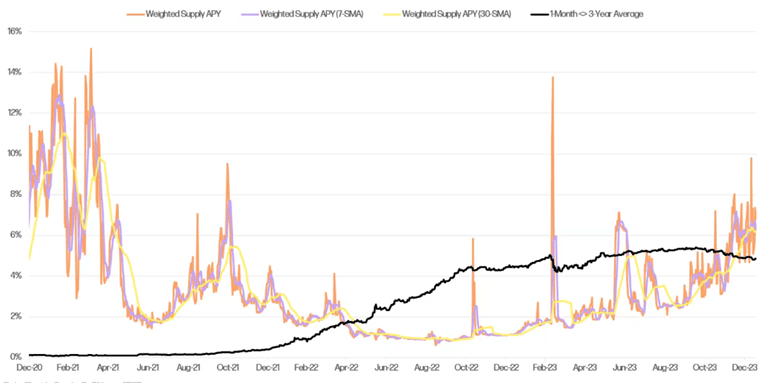

From Short Term Perspective: Fed’s rate hike pushing crypto investor seeking high yield product. The actions of the Federal Reserve have contributed heavily to the popularity of RWAs this year. Off-chain yield has become more attractive for on-chain users because of interest rate hikes. Additionally, the most valuable types of RWAs have changed as interest rates have increased.

Figure: US treasury rates against on-chain stablecoin supply APYs

Source: Galaxy Research, EMO Capital

4. Future Trends and Investment Opportunities in RWA

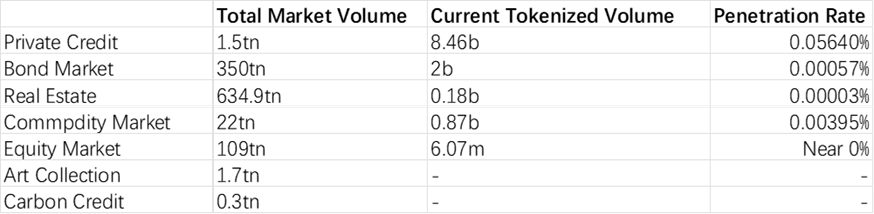

Even a slight increase on penetration over traditional assets means a huge growth in total RWA volume. While the RWA market is experiencing rapid growth in terms of size, its penetration rate remains very low compared to the massive scale of traditional assets. This implies that even the slightest increase in penetration rate translates into rapid market size growth. According to BCG Group, RWA sector market size will reach $1.8tn in 2030, indicating a huge growth room.

Table: RWA penetration on traditional asset classes (in USD)

Source: RWA.xyz, Bloomberg, Statista and others, EMO Capital

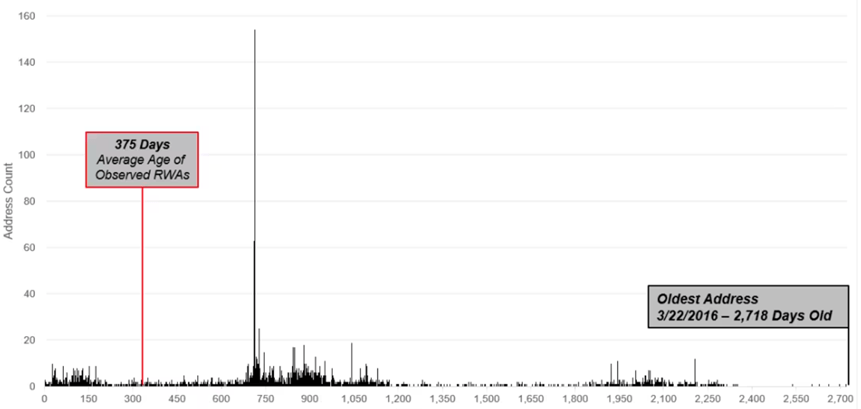

Attracting more traditional investors will be the key, but how? Most of the on-chain demand for RWAs is driven by a small number of native crypto users, as opposed to new crypto adopters or traditional investors moving on-chain. The average age of user addresses interacting with RWA tokens predates the creation of these assets on-chain, and highlights that the average RWA holder has already been transacting on-chain for some time.

According to Galaxy Research, many RWA holders that are highlighted above as having executed their first transaction less than one year ago are RWA holders of assets issued by Franklin Templeton and WisdomTree, indicating that the RWA products created by veteran financial firms may be succeeding in on boarding a newer suite of users into crypto, though the majority of RWA users still appear to be crypto-native users.

In the future, projects with ability to attract new users (traditional investors) have the opportunity to experience impressive growth, while the underlying issue still be how to build a regulated and trad-fi friendly framework.

Figure: Ages of addresses holding and interacting with RWAs in days

Source: Galaxy Research, EMO Capital

One of the challenges is, current on-chain data still cannot fully mitigate counterparties risk within transaction process. Although blockchain technology significantly improved the transparency of on-chain assets, blockchains are not natively designed to track unstructured or alternative data that exists off-chain, there still many types of data which are not fully reflect on RWA. Example as the financial situation of counter parties or quality of collaterals, and the authenticity of legal documents.

Meanwhile current crypto standard require fully transparency on underlying assets, however RWA like real-estate or art collections may contain many sensitive information which may not able to achieve full disclosure. This becomes another obstacle in term of on-chain off-chain integration.

Currently intermediaries between on-chain and off-chain are mainly tech companies. For example, Oracles fetch off-chain data such as asset prices, property values, or even legal documents and securely push these data points onto a blockchain. This data can then be used by smart contracts to trigger actions, automate processes, and ensure transparency in private credit transactions. However, the technological robustness and reliability of oracles have not yet been achieved. Innovation on on-chain off-chain data integration and optimization still have tremendous rooms to growth in future.

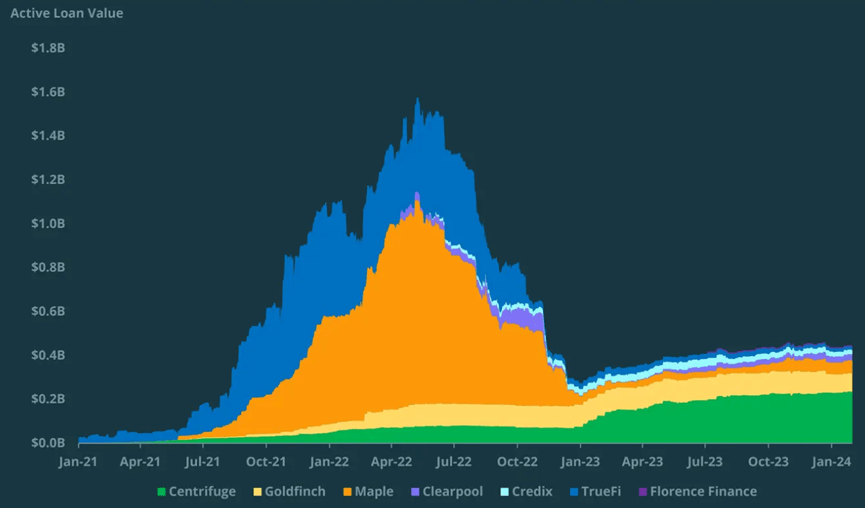

Figure: TVL of major RWA private credit protocol experience drop-off in 2022

Source: CoinGecko, EMO Capital

The solution of data integration may point to a new infrastructure design for RWA. To the existing obstacles as we discussed above, a RWA featured Layer1 infrastructure may set up a more advanced standards that provide better fit for information sensitivity of underlying asset meanwhile allow enhanced transparency in counterparties risk disclosure. Besides better integration of on-chain and off-chain information, another important part needs to be integrated will be the enforcement of off-chain actions, to achieve this, ideal infrastructure for RWA should build more connection with regulatory authorities so that actions like off-chain asset liquidation is feasible.

In fact, many innovative programs already start to reach this objective, example as Provenance blockchain, which is a layer 1 that is purpose-built to seamlessly and securely issue, transact, and service digitally-native financial assets at scale, they have incorporated Smart Contracting Engine and Off-chain Client-side Agreements into their core mechanism (according to their developer website). Nowadays Provenance has a total AUM of $13B, ranking as No1 in blockchain RWA TVL.

Another issue would be regulatory ambiguity, which require further improvement form policy makers. In most countries today, there exists a lack of clear regulation to govern the tokenization and securitization of real-world assets, regulatory ambiguity nowadays has prevented traditional investors set foots in RWA. In many countries RWA underlying assets are recognized as Securities, which means they are strictly under many juristic controls. Nowadays only Switzerland allow issuance of securitized RWA through DLT Act (Distributed Ledger Technology Act), other countries legislation still exist ambiguity.

Many projects achieve innovation in current legal framework, but further growth requirement legislation improvement. For example, Backed Finance use a tool called bearer instruments allow qualified institution resell their tokenized product to retail investors, expanding the scope of demand. However these innovations are just reforms based on current legislation framework, the true growth opportunities laid besides the improvement of legislation on RWA.

5. Conclusion

This research highlights the significant potential and future trends of Real-World Assets within the DeFi ecosystem. Despite experiencing rapid growth, the RWA market’s penetration remains minimal compared to traditional assets, indicating that even a slight increase in adoption could lead to substantial expansion. The integration of RWAs into DeFi not only enhances asset accessibility and liquidity but also introduces stability to the volatile crypto market. However, challenges such as technological robustness, regulatory clarity, and the need for innovative infrastructure to bridge on-chain and off-chain data persist. The market’s trajectory suggests a vast opportunity for growth, contingent upon attracting traditional investors and overcoming current obstacles through legislative advancements and technological innovation.